U.S. Physical Security Market Summary

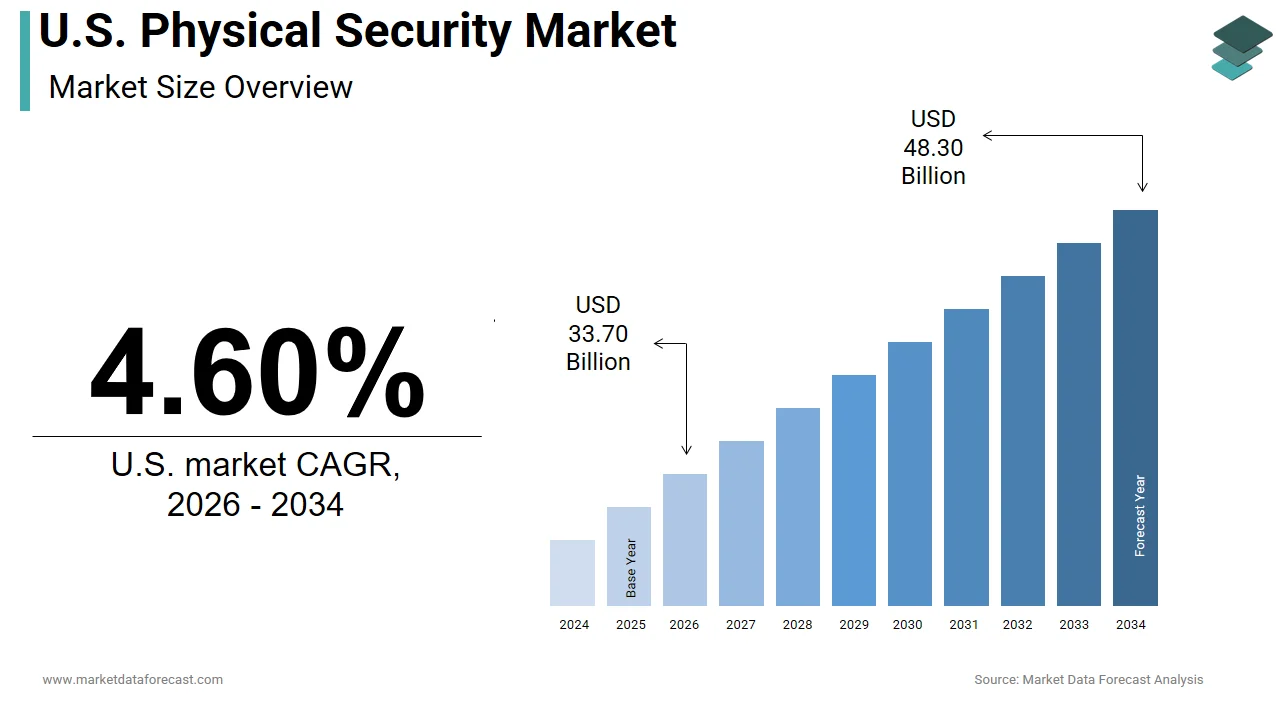

The U.S. physical security market was valued at USD 30.80 billion in 2024, is estimated to reach USD 32.22 billion in 2025, and is projected to reach USD 46.17 billion by 2033, growing at a CAGR of 4.60% from 2025 to 2033. The growth of the U.S. physical security market is driven by the rising need for asset protection, increasing security concerns across government and commercial facilities, integration of AI and IoT in surveillance systems, and expanding adoption of cloud-based access control solutions.

Key Market Trends

- Growing implementation of AI-enabled surveillance cameras and facial recognition technologies to enhance real-time threat detection.

- Increasing demand for cloud-based physical security solutions for scalable monitoring and analytics.

- Expanding integration of physical and cybersecurity frameworks for unified threat management.

- Rising deployment of access control systems, sensors, and video management software in commercial environments.

- Growing investments by the U.S. government in critical infrastructure protection and public safety systems.

Segmental Insights

- Based on component, the hardware segment accounted for 58.3% of the U.S. physical security market share in 2024, driven by the high adoption of surveillance cameras, sensors, alarms, and access control devices across public and private sectors.

- Based on end-user, the commercial/industrial vertical segment was the largest in 2024, reflecting the increasing emphasis on workplace safety, theft prevention, and facility monitoring in manufacturing, logistics, and retail facilities.

- Based on vertical, the government sector held 31.3% of the U.S. physical security market share in 2024, supported by continuous federal initiatives for homeland security, transportation safety, and critical infrastructure protection.

Competitive Landscape

The U.S. physical security market is highly competitive, with players focusing on AI integration, cloud analytics, and unified security platforms. Strategic collaborations, product innovation, and expansion into managed security services are key strategies among leading firms. Prominent players dominating the market include Honeywell International Inc., Axis Communications AB, Bosch Sicherheitssysteme GmbH, Hangzhou Hikvision Digital Technology Co., Ltd., Dahua Technology Co., Ltd, Johnson Controls, Cisco Systems, Inc., SECOM CO., LTD., ADT, Genetec Inc., Anixter International, Inc., Allied Universal Security Services LLC, Senstar Corporation, NordLayer, Evolv Technology, Cloudvue, Ava Security, Acura, Verkada Inc., and SEAtS Software.

U.S. Physical Security Market Size

The size of the U.S. physical security market was worth USD 30.80 billion in 2024. The market is anticipated to grow at a CAGR of 4.60% from 2025 to 2033 and be worth USD 46.17 billion by 2033 from USD 32.22 billion in 2025.

The physical security was the integrated deployment of hardware, software, and human protocols designed to deter, detect, delay, and document unauthorized physical access to assets, facilities, and personnel across public and private domains.

MARKET DRIVERS

Rising Physical Intrusions Mandating Security Infrastructure Upgrades

The escalating frequency of targeted physical intrusions against corporate and institutional facilities is greatly influencing the growth of the U.S. physical security market. This trend has triggered mandatory security upgrades under insurance underwriting guidelines. Many commercial property policies issued in 2023 now require verified video alarm systems and dual-authentication access for claim eligibility.

Federal Cyber-Physical Security Convergence Mandates Strengthening Market Growth

The federal mandate for convergence between cybersecurity and physical security postures under Executive Order 14028. The National Institute of Standards and Technology’s SP 800-53 Rev. 5 framework now explicitly requires biometric liveness detection at all Tier-3 facility entry points by affecting over 12,000 federal sites and their subcontractors.

MARKET RESTRAINTS

Shortage of Certified Integrators Hindering Converged Security System Deployment

The acute shortage of certified physical security integrators capable of deploying converged cyber-physical systems is restricting the growth of the U.S. physical security market. The Bureau of Labor Statistics projects only 3.1% annual growth in security installer employment through 2030, insufficient to meet deployment mandates from federal infrastructure bills.

Biometric Data Privacy Laws Creating Compliance Fragmentation Across States

The legal ambiguity surrounding biometric data collection at private facilities in states with stringent consent laws is also hindering the growth of the U.S. physical security market. The California Privacy Protection Agency’s draft regulations now classify palm-vein scans as “sensitive biometric identifiers,” requiring opt-in consent even for employee access. These jurisdictional inconsistencies force national enterprises into fragmented compliance architectures, which involve deploying different systems in different states.

MARKET OPPORTUNITIES

Expansion of AI-Enabled Perimeter Intrusion Detection Systems Across U.S. Military Installations

AI-enabled perimeter intrusion detection across all 498 domestic military installations by 2027 is substantially to create new opportunities for the growth of the U.S. physical security market. As per the Pentagon’s 2024 Force Protection Directive, systems must fuse thermal imaging, seismic sensors, and drone-based reconnaissance into a single command dashboard by creating demand for open-architecture platforms compliant with DoD’s Unified Facilities Criteria 4-021. Contractors meeting these specifications gain entry into a procurement pipeline insulated from commercial budget cycles.

Federal Investment in Interoperable School Safety Infrastructure Driving Product Innovation

The retrofitting of K-12 school campuses under the Biden Administration’s $1 billion School Safety National Initiative is hindering the growth of the U.S. physical security market. The initiative prioritizes funding for systems that synchronize door lockdowns, visitor management, and gunshot detection, not as siloed products, but as interoperable platforms. Manufacturers offering FERPA-compliant cloud dashboards with role-based access for teachers, administrators, and first responders are capturing multi-year district-wide contracts.

MARKET CHALLENGES

Counterfeit Security Hardware Undermining System Integrity and Market Growth

The destabilizing deployment integrity is the proliferation of counterfeit physical security hardware infiltrating U.S. supply chains, particularly access control panels and camera enclosures. This attribute is a major factor that hinders the growth of the U.S. physical security market. Unlike software, compromised hardware cannot be patched remotely, and entire installations must be physically replaced.

Legacy Infrastructure Limiting Integration of Modern Security Systems

The architectural incompatibility of modern security systems with legacy building infrastructure in urban historic districts is restricting the growth of the U.S. physical security market. This constraint forces security designers into bespoke engineering solutions, fragmenting scalability.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Component, End-user, Type, Vertical, and Region. |

|

Various Analyses Covered |

Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

|

Market Leaders Profiled |

Honeywell International Inc. (U.S.), Axis Communications AB (Sweden), Bosch Sicherheitssysteme GmbH (Germany), Hangzhou Hikvision Digital Technology Co., Ltd. (China), Dahua Technology Co., Ltd. (China), Johnson Controls (Ireland), Cisco Systems, Inc. (U.S.), SECOM CO., LTD. (Japan), ADT (U.S.), Genetec Inc. (Canada), Anixter International, Inc. (U.S.), Allied Universal Security Services LLC (U.S.), Senstar Corporation (Canada), NordLayer (U.S.), Evolv Technology (U.S.), Cloudvue (U.S.), Ava Security (U.K.), Acura (Japan), Verkada Inc. (U.S.), SEAtS Software (Ireland). |

SEGMENTAL ANALYSIS

By Component Insights

The hardware segment accounted in holding 58.3% of the U.S. physical security market share in 2024, which is structurally embedded hardware forming the non-negotiable physical layer. Additionally, the Insurance Institute for Business & Home Safety mandates impact-resistant camera housings for all properties in hurricane-prone zones, which is driving volume through regulatory compulsion rather than discretionary upgrade, a demand vector that software alone cannot replicate.

The services segment is growing with an anticipated CAGR of 12.4% during the forecast period, with the operational complexity of converged cyber-physical deployments. Simultaneously, the Department of Defense’s Unified Facilities Criteria 4-021 mandates quarterly red-teaming and vulnerability assessments for all cleared facilities, institutionalizing recurring revenue for certified third-party auditors.

By End-user Insights

The commercial/industrial vertical segment was the largest by accounting for a significant share of the U.S. physical security market in 2024. As per the Federal Financial Institutions Examination Council requires dual-factor biometric authentication is required at all bank vault access points with a specification driving $1.2 billion in annual hardware refresh cycles per the American Bankers Association’s compliance expenditure audit.

The biometrics & access control systems segment is likely to grow with an expected CAGR of 14.1% during the forecast period, with the federal workforce mandates that the Office of Personnel Management’s 2023 directive requires all federal employees and contractors to transition to PIV-compliant biometric badges by 2026, affecting 4.2 million personnel.

By Vertical Insights

The government sector was the largest and held 31.3% of the U.S. physical security market share in 2024. The Cybersecurity and Infrastructure Security Agency’s Physical Security Baseline requires all federal facilities to implement PSIM-integrated command centers, where a mandate affecting 372,000 buildings under GSA stewardship.

The healthcare vertical is expected to register a CGAR of 15.7% throughout the forecast period. Simultaneously, the biometric access logs for all Schedule II narcotics storage affect 6,800 hospitals and 12,400 outpatient clinics. The healthcare security is tied to patient safety metrics with a linkage that embeds expenditure into accreditation requirements and malpractice risk mitigation, ensuring non-discretionary, regulation-locked growth regardless of economic headwinds.

REGIONAL ANALYSIS

California Market Analysis

California physical security market held 15.3% of the share in 2024 owing to the state’s unique regulatory architecture. Simultaneously, wildfire evacuation protocols require automated lockdown and remote camera activation in 12,000 critical facilities, with a specification absent in non-fire-prone states, by creating a compliance-driven demand stream unmatched in volume or complexity.

Texas Market Analysis

Texas was positioned second by capturing 10.1% of the U.S. physical security market share in 2024, with the petrochemical and border security imperatives. Simultaneously, the Department of Public Safety’s Operation Lone Star has deployed 3,200 AI-enabled border surveillance towers since 2021, each integrated with ground sensors and drone response triggers.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. physical security market include

- Honeywell International Inc. (U.S.)

- Axis Communications AB (Sweden)

- Bosch Sicherheitssysteme GmbH (Germany)

- Hangzhou Hikvision Digital Technology Co., Ltd. (China)

- Dahua Technology Co., Ltd (China)

- Johnson Controls (Ireland)

- Cisco Systems, Inc. (U.S.)

- SECOM CO., LTD. (Japan)

- ADT (U.S.)

- Genetec Inc. (Canada)

- Anixter International, Inc. (U.S.)

- Allied Universal Security Services LLC (U.S.)

- Senstar Corporation (Canada)

- NordLayer (U.S.)

- Evolv Technology (U.S.)

- Cloudvue (U.S.)

- Ava Security (U.K.)

- Acura (Japan)

- Verkada Inc. (U.S.)

- SEAtS Software (Ireland)

MARKET SEGMENTATION

This research report on the U.S. physical security market has been segmented and sub-segmented into the following categories.

By Component

- Hardware

- Software

- Services

By End-user

- Residential

- Commercial/Industrial

- Small and Medium-sized Enterprises

- Large Enterprises

By Type

- Video Surveillance Systems

- Biometrics & Access Control Systems

- Intrusion Detection and Prevention Systems

- Fire Detection Systems

- Physical Security Information Management (PSIM)

- Others (Physical Identity and Access Management, etc.)

By Vertical

- BFSI

- Government

- Healthcare

- Manufacturing

- Retail

- Transportation & Logistics

- Energy & Utilities

- Others (Education, Sports, etc.)

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

link