Global Fitness App Market Size

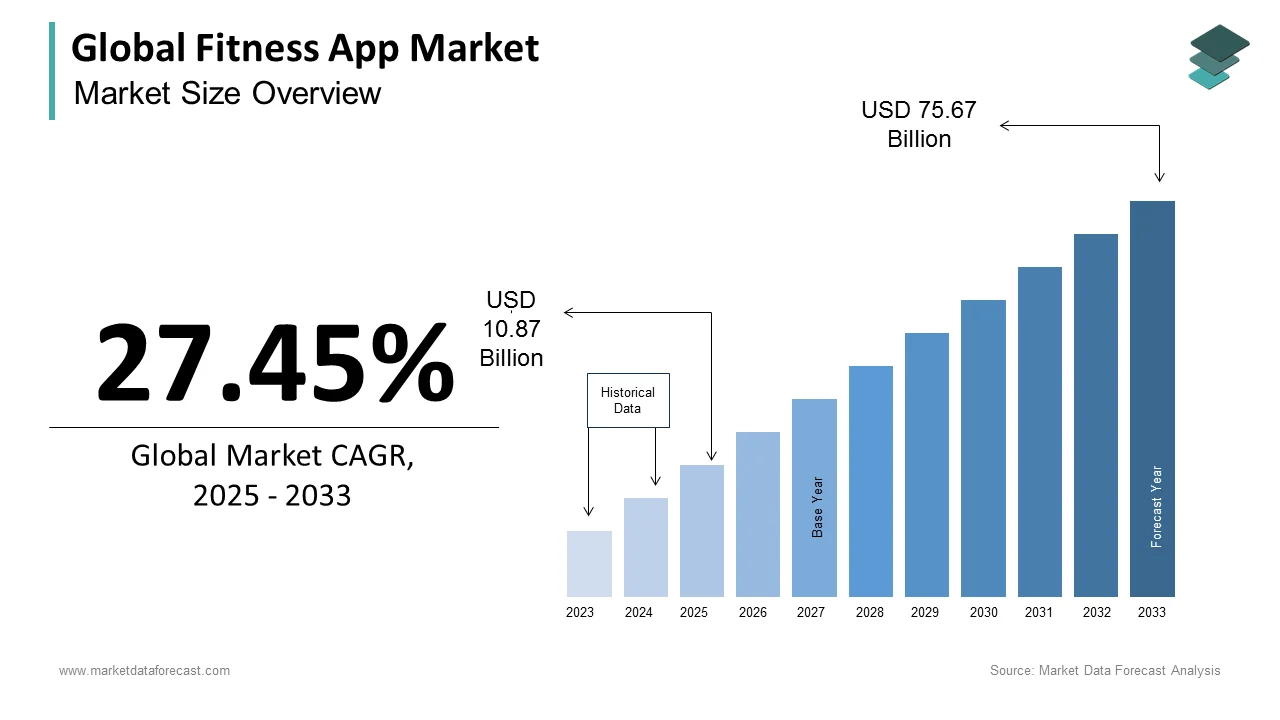

The global fitness app market was worth USD 8.53 billion in 2024 and is anticipated to reach a valuation of USD 75.67 billion by 2033 from USD 10.87 billion in 2025. It is predicted to register a CAGR of 27.45% during the forecast period 2025-2033.

The Fitness App supports physical wellness through guided workouts, nutritional planning, activity tracking, and behavioural motivation, which is primarily delivered via smartphones and wearable integrations. These applications function across diverse segments, including weight management, strength training, yoga, cardio, and mental well-being, leveraging artificial intelligence and biometric feedback to personalise user experiences. The proliferation of health-conscious consumerism, particularly in urbanised regions, has catalysed demand for accessible, self-directed fitness solutions. As per the World Health Organization, over 1.4 billion adults globally fail to meet recommended physical activity levels by creating a compelling public health imperative that fitness apps are increasingly positioned to address.

MARKET DRIVERS

Rising Prevalence of Sedentary Lifestyles Driving Demand for Fitness Apps

The escalating global prevalence of sedentary behaviour in urban populations where desk-based occupations and prolonged screen time have become normative is driving the growth of the Fitness App Market. The shift toward home-based employment has reduced incidental physical activity, with Stanford University research indicating that the average office worker’s daily step count declined by nearly 40% during peak remote work periods. This behavioural shift has intensified consumer reliance on digital fitness solutions to compensate for lost movement. As per the U.S. Bureau of Labor Statistics, the average American spends over 9 hours daily in sedentary activities, underscoring a structural gap that fitness technologies aim to bridge. Moreover, longitudinal data from the Global Observatory for Physical Activity confirms that countries with higher urbanisation rates, such as South Korea and Singapore, report the lowest physical activity compliance, directly correlating with higher adoption rates of mobile fitness platforms. The integration of gamification and real-time feedback in apps like MyFitnessPal and Fitbod enhances adherence, addressing the psychological inertia associated with inactivity.

Increasing Integration of Wearable Technology Enhancing App Efficacy

The deepening synergy between fitness applications and wearable health technology, by enabling real-time biometric monitoring and data-driven personalisation, is additionally escalating the growth of the Fitness App Market. As per the International Data Corporation, global wearable device shipments reached 189 million units in 2023, reflecting widespread consumer acceptance and infrastructure readiness for app integration. Apple, a dominant player in the wearables space, reported in its 2023 earnings commentary that over 200 million active users engage with its Health ecosystem, most of whom synchronise data with third-party fitness applications. This interoperability fosters a closed-loop system where user behaviour informs algorithmic adjustments, increasing engagement and long-term retention. Research published in Nature Digital Medicine demonstrates that users of fitness apps connected to wearables exhibit 35% higher adherence rates over six months compared to standalone app users. Additionally, Google’s acquisition of Fitbit and subsequent integration into its Pixel Watch platform illustrates the strategic prioritisation of ecosystem cohesion.

MARKET RESTRAINTS

Data Privacy Concerns Hindering Consumer Trust and Adoption

The growing apprehension surrounding data privacy and the unauthorised use of sensitive health information is restricting the growth of the Fitness App Market. Many fitness applications collect granular personal data, including location history, biometric readings, and even menstrual cycles, raising ethical and regulatory concerns. As per a 2023 investigation by the Norwegian Consumer Council, 60% of popular fitness apps share user data with third-party advertisers without explicit informed consent, often bypassing standard privacy safeguards. This practice has triggered regulatory scrutiny, particularly under frameworks like the General Data Protection Regulation (GDPR) in Europe, where several app developers have faced fines for non-compliance. According to the U.S. Federal Trade Commission, a 75% increase in consumer complaints related to health app data misuse between 2021 and 2023, indicating escalating public distrust.

Limited Efficacy and User Retention Challenges in Long-Term Engagement

The persistent issue of low long-term user engagement and questionable clinical efficacy of many is degrading the growth of the Fitness App Market. This attrition is attributed to generic content, lack of personalisation, and insufficient behavioural support mechanisms. The University of Pennsylvania’s Centre for Health Incentives and Behavioural Economics found that apps relying solely on automated reminders and static workout plans fail to sustain motivation, particularly among users with pre-existing health conditions. Additionally, a meta-analysis by The BMJ concluded that only 28% of commercially available fitness apps are developed in consultation with healthcare professionals, raising concerns about the scientific validity of their recommendations. In low- and middle-income countries, where digital literacy and smartphone penetration are still evolving, the usability gap further exacerbates disengagement. UNESCO reports that in Southeast Asia, nearly 40% of adult smartphone users lack the proficiency to navigate complex health applications effectively. Moreover, the absence of regulatory oversight for app content means users may follow regimens that are either ineffective or potentially harmful.

MARKET OPPORTUNITIES

Expansion into Corporate Wellness Programs Creating Scalable Demand

The integration of fitness applications into corporate wellness initiatives, where employers are increasingly investing in digital health platforms to enhance employee productivity and reduce healthcare expenditures, is solely to create huge opportunities for the growth of the Fitness App Market. Chronic diseases linked to physical inactivity cost the global economy an estimated $68 billion annually in lost productivity, as reported by the World Economic Forum. In response, multinational corporations are adopting preventive health strategies, with fitness apps serving as cost-effective tools for large-scale employee engagement. As per the International Labour Organization, over 60% of Fortune 500 companies now offer digital wellness platforms as part of their benefits package, a trend accelerating in Asia-Pacific and North America.

Personalised AI-Driven Coaching Enabling Hyper-Targeted Fitness Solutions

The advancement of artificial intelligence will deliver hyper-personalised coaching that adapts to individual physiology, lifestyle, and behavioural patterns, which shall also pose new opportunities for the growth of the Fitness App Market. Platforms like Freeletics and Future use machine learning to modify exercise intensity based on real-time performance feedback, resulting in 45% higher user satisfaction compared to static programs, according to a clinical trial conducted by the German Sports University in Cologne. The integration of natural language processing enables conversational coaching, simulating human trainer interactions. Google’s AI research team demonstrated that users engaging with AI coaches showed a 29% improvement in workout consistency over 12 weeks.

MARKET CHALLENGES

Regulatory Fragmentation Impeding Global App Standardisation

The absence of harmonised regulatory frameworks governing health claims, data usage, and clinical validation across jurisdictions is impeding the growth of the Fitness App Market. As per the World Health Organization’s 2023 Digital Health Regulation Survey, only 22 out of 194 member states have established specific guidelines for fitness and wellness applications, leaving developers in legal grey zones. This regulatory asymmetry complicates global expansion, particularly for startups lacking resources to navigate divergent compliance requirements. Furthermore, the lack of universal efficacy standards means that apps with unproven benefits can be marketed alongside clinically validated tools, diluting consumer trust.

Digital Divide Limiting Access in Low-Income and Rural Populations

The low-income, rural, and elderly populations, with the inclusivity of digital wellness, are expected to hinder the growth of the Fitness App Market. Despite global smartphone penetration reaching 67%, as reported by the International Telecommunication Union, significant disparities persist in internet reliability, device affordability, and digital literacy. This infrastructure gap prevents equitable engagement with fitness apps, which often require continuous data streaming and advanced hardware. Moreover, older adults, among the most in need of structured physical activity, are disproportionately excluded. Language barriers further exacerbate exclusion; only 12% of top fitness apps offer content in indigenous or regional languages, as per Ethnologue’s 2023 assessment. Without targeted design and policy interventions, the fitness app market risks becoming a privilege of urban, affluent, and technologically literate demographics, contradicting its public health potential.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Type, Platform, Application/User Type, End-User, Revenue Model, and Region. |

|

Various Analyses Covered |

Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

|

Market Leaders Profiled |

MyFitnessPal Inc., Motorola Mobility LLC, Azumio, WillowTree, Inc., Under Armour, Dom and Tom, Grandapps, Fitbit, ASICS, WillowTree, Inc., and Appster. |

SEGMENTAL ANALYSIS

By Type Insights

The workout & exercise apps segment held 38.2% of the global fitness app market share in 2024 with its direct alignment with tangible fitness outcomes such as strength development, endurance improvement, and physique transformation, which remain primary motivators for app adoption. As per the NPD Group, sales of connected fitness equipment in the U.S. surged by 72% between 2021 and 2023, with Peloton, Tonal, and Mirror users predominantly relying on proprietary workout apps to deliver structured regimens. Additionally, the proliferation of hybrid fitness models blending in-person and digital training has elevated demand for flexible, on-demand content. Furthermore, platforms like Nike Training Club and Freeletics have leveraged celebrity trainer partnerships and AI-driven personalisation to expand reach, with Nike reporting over 50 million active users in 2023.

The meditation & Mindfulness apps segment is growing with an estimated CAGR of 26.4% in the coming years, owing to the rising global awareness of mental health and the integration of mindfulness into preventive healthcare strategies. According to the World Health Organization, depression and anxiety disorders cost the global economy $1 trillion annually in lost productivity, prompting employers, insurers, and governments to adopt digital mental wellness tools. In response, mindfulness apps such as Calm and Headspace have become central to corporate well-being programs, with Calm reporting integration into over 7,000 enterprise wellness platforms by 2023. A clinical trial published in JAMA Internal Medicine demonstrated that users of guided meditation apps experienced a 31% reduction in anxiety symptoms over eight weeks, lending scientific credibility to their efficacy. Additionally, younger demographics are embracing mindfulness as part of holistic self-care, with Common Sense Media revealing that 43% of adolescents in the U.S. use meditation apps to manage academic stress.

By Platform Insights

The Android segment was the largest by capturing a prominent share of the fitness app market in 2024, with the extensive penetration of Android devices in emerging and developing economies, where affordability and device variety. The open-source nature of Android also enables broader device compatibility by allowing fitness apps to function on low-cost smartphones with limited processing power, a crucial advantage in price-sensitive markets. A study by the Asia Pacific Journal of Public Health found that Android-based fitness app users in Thailand and the Philippines exhibited 25% higher engagement rates after the rollout of Health Connect, due to improved interoperability with wearables. Additionally, the Google Play Store’s less restrictive publishing policies facilitate faster app deployment and regional customisation, enabling developers to tailor content for local languages and cultural preferences. This accessibility, combined with Google’s expanding partnerships with telecom providers for zero-rated data plans that ensures Android remains the primary gateway for first-time digital fitness users worldwide.

The iOS platform segment is expected to grow with a CAGR of 18.7% in the coming years with the increasing affluence of iOS users and their higher willingness to pay for premium fitness content and subscriptions. The ecosystem’s tight integration between hardware, software, and services amplifies user engagement. Apple Watch owners, who number over 120 million globally as reported by IDC, are 3.2 times more likely to subscribe to fitness apps than non-wearable users, according to a 2023 analysis by the Journal of Medical Internet Research. The seamless synchronisation of workout data across iPhone, iPad, and Apple Watch creates a frictionless experience that encourages sustained usage.

By Application/User Type Insights

The weight loss segment was the largest by occupying 44.3% of the fitness app market share in 2024, with the escalating global burden of overweight and obesity. According to the World Health Organization, over 1.9 billion adults, with prevalence doubling since 1980. The urgency of this public health crisis has intensified consumer demand for accessible, self-directed weight management tools. Apps like Noom and MyFitnessPal have capitalised on this need by combining calorie tracking, behavioural psychology, and personalised coaching.

The Wellness & Meditation user segment is projected to register a CAGR of 25.8% during the forecast period, owing to the health perception, where consumers increasingly prioritise holistic well-being over isolated physical metrics. As per the Harvard T.H. Chan School of Public Health, 74% of adults in high-income countries now define health as a balance of mental, emotional, and physical states, a mindset that aligns with the integrative approach of wellness apps. Employers are also accelerating adoption; the Society for Human Resource Management found that 71% of U.S. companies have expanded mental wellness benefits since 2020, with 89% offering subscriptions to platforms like Headspace and Calm.

REGIONAL ANALYSIS

North America Market Analysis

North America was the largest contributor in the fitness app market with a 37.3% share in 2024. The United States is leading the highest growth of the Fitness App Market. According to the Pew Research Center, 85% of American adults own a smartphone, and 42% use health or fitness apps regularly, the highest rate globally. Additionally, the FDA’s Digital Health Pre-Cert Program has accelerated the validation of high-quality apps, enhancing consumer trust. The Canadian market, though smaller, mirrors this trend, with provincial health systems piloting app-based chronic disease management programs. As per Statistics Canada, over 30% of adults in Ontario and British Columbia use fitness apps to manage conditions like hypertension and diabetes.

Europe Market Analysis

Europe was positioned second by holding 28.3% of the share in 2024. Countries like Germany, the UK, and Sweden are at the forefront, integrating fitness apps into national health strategies to combat rising obesity and mental health issues. As per the European Commission’s eHealth Action Plan, 21 member states now recognise digital therapeutics as reimbursable services, enabling apps like Kaia Health to be prescribed for chronic pain management. Additionally, Nordic countries exhibit high engagement due to digital literacy and public investment in e-wellness; Finland’s Ministry of Social Affairs and Health notes that 48% of adults use fitness apps regularly, supported by municipal wellness subsidies.

Asia Pacific Market Analysis

Asia Pacific is swiftly emerging to showcase huge opportunities for the growth of the fitness app market during the forecast period. China, India, and South Korea are leading the regional charge, driven by rising disposable incomes, urbanisation, and government-backed digital health initiatives. As per the Asia Pacific Observatory on Health Systems and Policies, China’s “Healthy China 2030” strategy includes digital fitness as a core component, with over 300 million citizens already using health apps. Indian smartphone users, numbering 850 million, are increasingly adopting local platforms like Cult. Fit and HealthifyMe, which reported a 150% increase in premium subscriptions between 2022 and 2023, according to RedSeer Consulting.

Latin America Market Analysis

Latin America fitness app market growth is likely to grow with Brazil and Mexico serving as primary growth engines amid expanding digital inclusion and rising health awareness. Brazil, the largest market in the region, has seen a surge in fitness app downloads, with AppTweak reporting over 120 million installs in 2023, a 35% year-on-year increase. Local developers like Totalpass and SmartFit have introduced hybrid fitness models combining app access with gym memberships, achieving over 5 million subscribers collectively. In Colombia, the Ministry of Health has partnered with digital wellness platforms to deliver public health campaigns, particularly in underserved areas. However, challenges remain, including low credit card penetration and digital literacy gaps, as UNESCO reports that only 45% of rural populations can navigate complex apps.

Middle East and Africa Market Analysis

The Middle East and Africa fitness app market growth is likely to grow with nascent but rapidly evolving adoption patterns. The Gulf Cooperation Council (GCC) countries, particularly the UAE and Saudi Arabia, are spearheading digital health transformation as part of broader economic diversification agendas. As per the Dubai Health Authority, the UAE’s “Smart Dubai” initiative has integrated fitness apps into its city-wide wellness ecosystem, with over 1.2 million residents participating in government-backed fitness challenges in 2023. Saudi Arabia’s Vision 2030 includes a national physical activity strategy, aiming to increase daily exercise participation from 13% to 20% by 2030, with apps like Mawid and Sehaty playing a central role. In Africa, South Africa leads in digital fitness uptake, with Stats SA reporting that 28% of urban smartphone users engage with fitness apps regularly. However, widespread connectivity issues persist; the International Telecommunication Union indicates that only 38% of Africans use the internet, limiting scalability.

COMPETITIVE LANDSCAPE

The competition in the Fitness App Market is intensifying as global tech giants, specialised health startups, and traditional fitness brands converge on digital wellness. Differentiation increasingly hinges on personalisation, scientific validation, and ecosystem integration rather than basic functionality. Companies are investing heavily in AI-driven coaching, real-time biometric synchronisation, and behavioural psychology to enhance user adherence. Market leaders are expanding beyond standalone apps into holistic health platforms that encompass nutrition, mental well-being, and chronic disease management. Strategic acquisitions and partnerships with insurers, employers, and healthcare systems are enabling scalable distribution. Regional customisation is highly important in culturally diverse markets like Asia Pacific, where dietary habits and fitness preferences vary widely. Emerging players are challenging incumbents with niche offerings, such as women’s health or senior fitness, creating a fragmented yet dynamic landscape. Data privacy and regulatory compliance are becoming competitive differentiators, with transparent practices fostering consumer trust.

KEY MARKET PLAYERS

The major players operating in the global fitness app market profiled in this report are

- MyFitnessPal Inc.

- Motorola Mobility LLC

- Azumio

- WillowTree, Inc.

- Under Armour

- Dom and Tom

- Grandapps

- Fitbit

- ASICS

- Appster

TOP LEADING PLAYERS IN THE MARKET

MyFitnessPal is holding the top position in the fitness app market by leveraging its comprehensive nutrition and activity tracking capabilities. The platform’s extensive food database, available in multiple regional languages, caters to diverse dietary preferences across India, Japan, and Australia. In 2023, the company enhanced its integration with Google Fit, enabling seamless biometric synchronisation for Android users across the region. MyFitnessPal also launched culturally adapted meal plans for Southeast Asian markets, incorporating local cuisines to improve user relevance. The app introduced AI-powered meal logging and barcode scanning optimised for regional grocery products, increasing usability. Collaborations with health insurers in Australia and corporate wellness providers in Singapore have expanded its institutional reach.

Nike Training Club (NTC) has significantly influenced the Asia Pacific fitness app market by combining global brand authority with hyper-localised content strategies. The app offers customised workout programs featuring regional athletes and trainers from countries like China, South Korea, and India, enhancing cultural resonance. In 2023, Nike launched a series of short-form video workouts tailored for urban professionals in Tokyo, Mumbai, and Sydney, aligning with fast-paced lifestyles. The integration of NTC with Nike’s membership ecosystem enables seamless access to exclusive challenges and product rewards, driving sustained engagement. The company also partnered with fitness influencers across TikTok and Instagram in Southeast Asia to amplify visibility. In Japan, Nike collaborated with corporate wellness platforms to distribute NTC subscriptions through employer programs.

Noom has emerged as a key player in the Asia Pacific market by introducing behaviour-centric weight management programs grounded in cognitive behavioural therapy. The company expanded into Japan in 2022 and South Korea in 2023, localising its coaching content and hiring native-speaking psychologists to guide users through culturally sensitive dietary transitions. Noom’s AI-driven platform adapts feedback based on user emotional triggers, a feature that resonated strongly in high-stress urban environments like Seoul and Tokyo. The company partnered with Japanese health insurers to offer subsidised subscriptions, increasing accessibility. In India, Noom conducted pilot programs with corporate clients in Bengaluru and Hyderabad to address rising metabolic health concerns.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Fitness App Market are deploying advanced personalisation, strategic partnerships, AI integration, ecosystem expansion, and regional customisation to consolidate their positions. Companies are leveraging artificial intelligence to deliver adaptive workout and nutrition plans based on biometric feedback and behavioural patterns. Localisation of content, including language, cuisine, and trainer representation, strengthens engagement in diverse markets. Subscription bundling and gamification techniques improve retention. Additionally, regulatory compliance and clinical validation are being prioritised to position apps as legitimate health interventions in regions with evolving digital health policies.

GLOBAL FITNESS APP MARKET NEWS

- In January 2023, MyFitnessPal launched AI-powered meal logging with regional food recognition for users in India, Indonesia, and Australia by enhancing dietary tracking accuracy and user engagement across Asia Pacific.

- In March 2023, Nike introduced localized workout programs on Nike Training Club featuring trainers from Japan, South Korea, and India, which is increasing cultural relevance and adoption in key urban markets.

- In June 2023, Noom partnered with Japanese health insurer Sompo Japan to offer subsidized subscriptions by integrating its behavioural weight management program into corporate wellness plans.

- In September 2023, Fitbit, under Alphabet, integrated its health data platform with public healthcare systems in Singapore and Thailand by enabling fitness app data to support preventive care initiatives.

- In February 2024, HealthifyMe, a leading Indian fitness app, launched an AI-powered virtual coach named “Reeta” in Hindi and Tamil, which is expanding accessibility and deepening user engagement in non-English speaking regions.

MARKET SEGMENTATION

This market research report on the global fitness app market has been segmented and sub-segmented based on the type, platform, device, and region.

By Type

- Activity Tracking Apps

- Nutrition & Diet Apps

- Workout & Exercise Apps

- Meditation & Mindfulness Apps

- Others (e.g., Sleep Tracking, Health Monitoring)

By Platform

- iOS

- Android

- Others (e.g., Windows, Web-based)

By Application/User Type

- Weight Loss

- Muscle Building

- Wellness & Meditation

- General Fitness

- Sports & Training

- Rehabilitation & Physical Therapy

By End-User

- Individual Consumers

- Fitness Centers & Gyms

- Healthcare Providers

- Corporate Wellness Programs

By Revenue Model

- Freemium

- Subscription-Based

- Advertisement-Based

- One-Time Purchase

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

link