Strengthening South Korea’s Global Value Chain Through Increased Robot Adoption

Published October 28, 2024

In the early 21st century, global value chains (GVCs) grew longer and became reliant on low-cost countries for assembly, employing just-in-time production methods. These practices were tested during events like the US-China trade war and the COVID-19 pandemic. In response, many companies shifted their GVC strategies toward a focus on resilience and diversification. As this transition from “just-in-time” to “just-in-case” planning takes place, it is crucial to assess South Korea’s current position in these global chains. As a result, a natural question arises about whether South Korea is doing enough to achieve the just-in-case strategy, in particular with the integration of industrial robots.

South Korea’s GVC Participation and Position

Industries depend on one another for goods and services in the production process, illustrating their economic interdependence. Backward and forward linkages help measure these connections by showing how changes in one industry’s output can affect others. For example, an increase in processor chip production drives up demand for inputs like utilities and wafer manufacturing (backward linkages) while also supplying more components to downstream sectors such as computer manufacturing (forward linkages). GVC participation can be quantified by assessing a country’s share of forward and backward linkages in its total trade. Additionally, GVC position can be determined by dividing the length (number of stages) of forward linkages by the length of backward linkages. A higher position index suggests a more downstream role, while a lower value indicates an upstream placement.

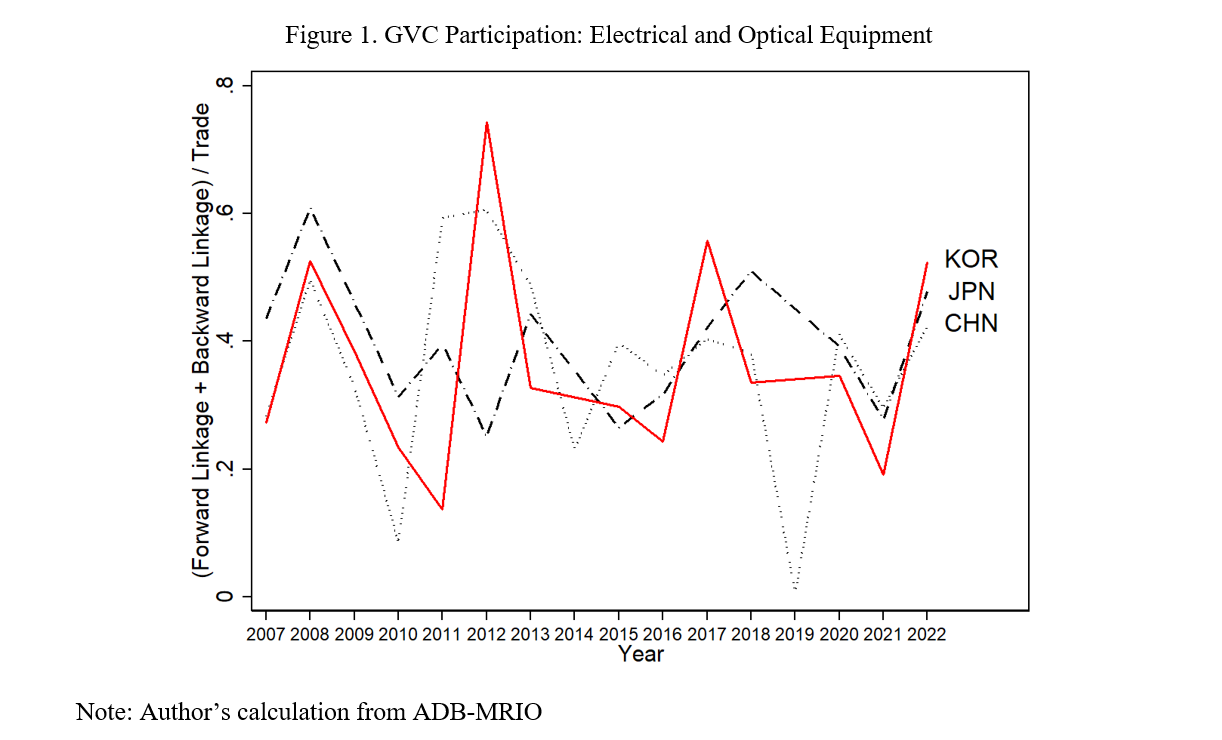

The Asian Development Bank’s Multi-Regional Input-Output (ADB-MRIO) database helps to assess South Korea’s GVC participation and position from 2007 to 2022. In the electrical and optical equipment sector, which includes electronics manufacturing, South Korea’s participation has been on the rise since 2021, as indicated in Figure 1. Over half of Korea’s trade in this sector involves GVCs, surpassing both China and Japan. Similarly, Figure 2 shows that South Korea’s participation rate in the transport equipment sector, which covers automobile manufacturing, is also around 50 percent, again higher than China and Japan. These figures indicate that South Korean firms in these sectors (e.g., Samsung and Hyundai) rely on outsourcing and offshoring for much of their production, much more so in 2022 than in 2021 or 2020. Given that companies like Samsung and Hyundai are integrated with China and Japan for their GVC activities, we are observing more—not less—interlinking among the three Asian nations. It implies more intensified regionalization as companies shift toward just-in-case planning, such as the South Korea-China-Japan interlinkage or the US-Mexico-Canada Agreement (USMCA) in 2020. This near-shoring pattern based on geography or friend-shoring pattern based on geopolitical alignment may be the outcome of the just-in-case strategy. So, for companies like Samsung and Hyundai, a natural transition is greenfield foreign direct investment in North America to be included in the USMCA when they look outside Asia.

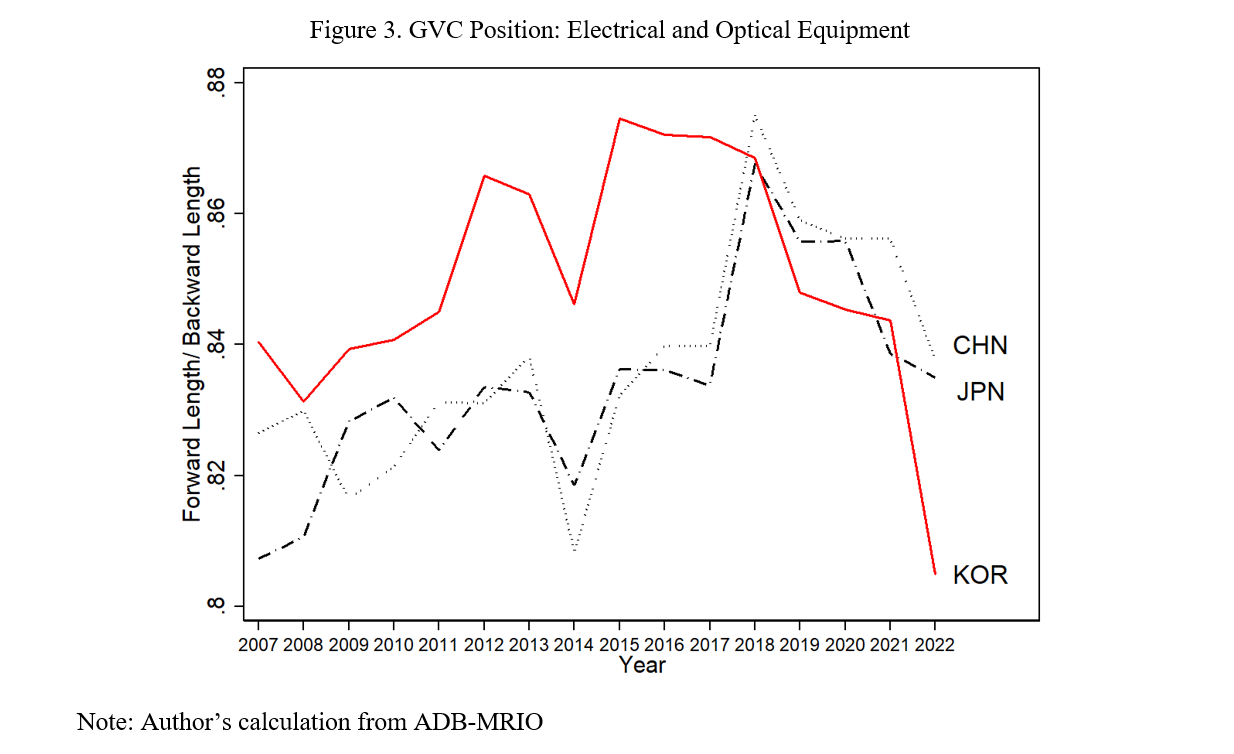

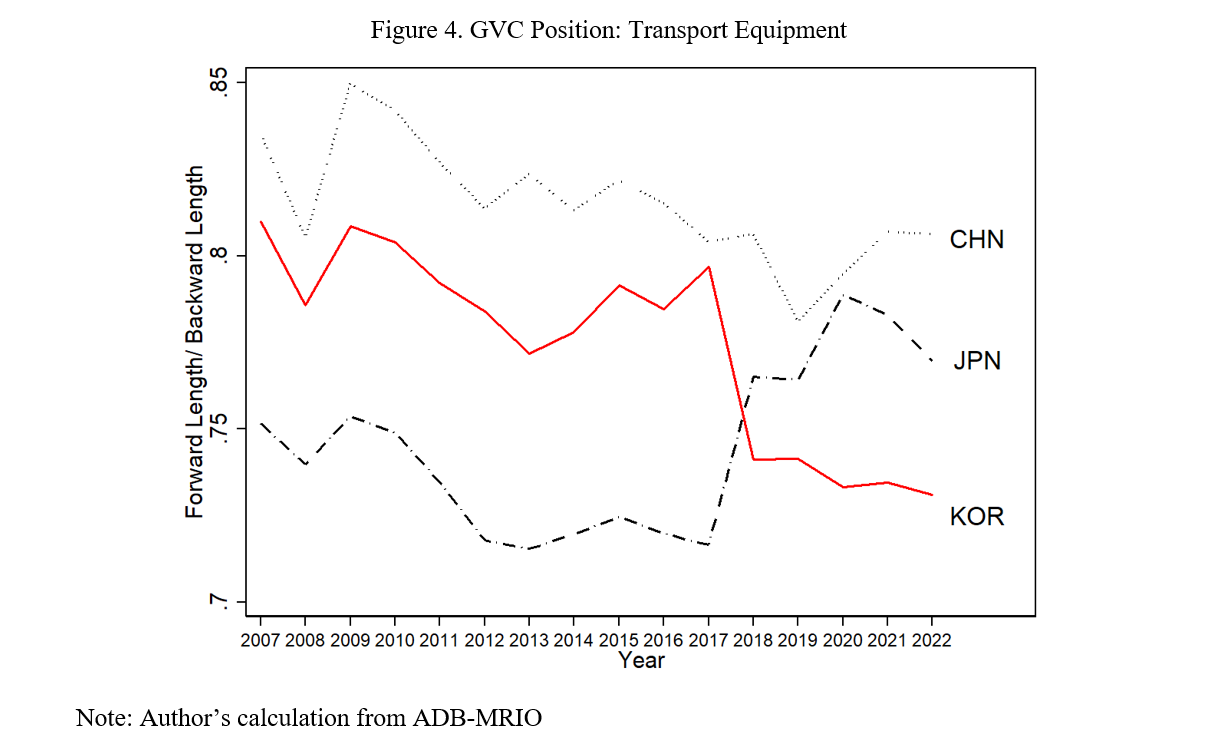

Figure 3 highlights that South Korea’s recent GVC position in the electrical and optical equipment sector has shifted more upstream. The ratio dropped from 0.87 in 2015 to 0.81 in 2022, reflecting a placement further from the final stages of production than China or Japan. A notable decline occurred around 2018, which aligns with the US-China trade war. In the transport equipment sector, shown in Figure 4, South Korea’s position also trends upstream, with a sharp decline in 2017, in contrast to Japan’s increase during the same period.

In all, South Korea’s participation in GVCs has been growing, particularly in critical sectors such as electronics and automobiles. However, its position has become more upstream, especially after 2018, indicating that its manufacturing activities are now further from the final stages of consumption. This shift emphasizes the importance of quality control in production processes. With rising GVC involvement and a focus on the latter stages of manufacturing, building resilient supply chains and maintaining consistency in the assembly is vital. This is where the integration of industrial robots could play a significant role, but is South Korea doing enough?

Industrial Robot Adoption

The International Federation of Robotics (IFR) provides key data on global installations of industrial robots. According to their latest figures, five countries—China (52 percent), Japan (9 percent), the United States (7 percent), South Korea (6 percent), and Germany (5 percent)—accounted for 79 percent of the 437,599 robots installed worldwide in 2022.

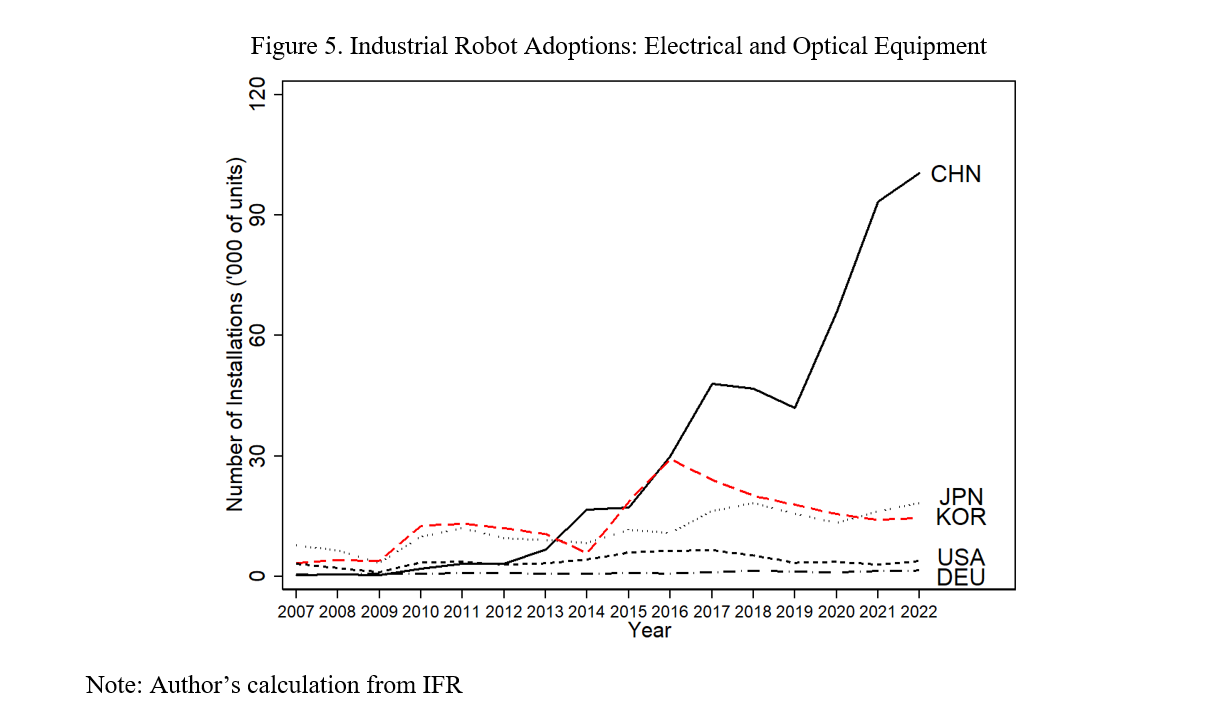

Using the IFR database, Figures 5 and 6 illustrate South Korea’s robot adoption rates in the electrical and optical equipment and transport equipment sectors from 2007 to 2022, compared to other leading nations. China has shown the fastest rate of adoption in recent years. Although South Korea outpaced China and Japan before 2013, it now lags behind both countries in the electronics industries. In 2022, approximately 15,000 new robots were delivered to South Korea’s electronics sector and 10,000 to its automotive industry. These numbers are similar to the figures from 2010, indicating a stagnant adoption rate when compared to other countries.

We can point to industrial policies—or lack thereof—as the reason behind the different rates of industrial robot adoptions in China and South Korea. In 2015, President Xi Jinping announced a key industrial policy called “Made in China 2025” to promote technological advancement in the semiconductor and electronics industries. In 2020, China initiated another industrial policy called “New Energy Vehicle Industry Development Plan 2021-2035” for the automotive industry to transition the country into the frontier for electric vehicles. Hence, we observe corresponding spikes in each sector (2015 for Figure 5 and 2020 for Figure 6).

Policy Suggestions

South Korea’s strong engagement in GVCs contrasts with its relatively slow embrace of industrial robots. To enhance its international competitiveness, policies should be designed to speed up technological integration. These measures can position South Korea to leverage automation more effectively, strengthen its GVC presence, and bolster its export quality and manufacturing resilience. Here are some targeted policy actions:

1. Subsidies: Providing financial incentives, such as tax breaks, subsidies, or low-interest financing, could encourage firms to invest in robotics. Lowering the financial burden will help stimulate a quicker uptake of these technologies across various industries. As we have seen from China’s industrial policies in 2015 and 2020, subsidies are critical factors for increased industrial robot adoption. Some analysts estimate that China’s subsidy amount could be up to 4.9 percent of China’s GDP, which far surpasses any other nation’s spending on industrial policy.

2. Support Research, Development, and Innovation: Increased government investment in research and development within the robotics field, along with grants and partnerships with industry leaders, can drive innovation. Focusing on developing advanced, customized robotic solutions will benefit South Korea’s major industrial sectors.

3. Complementary Labor Policy: As companies adopt more industrial and service robots, the labor force will likely be disrupted. In the United States, one additional robot per one thousand workers decreased the employment-to-population share by 0.2 percentage points and wages by 0.42 percent. South Korea may face similar challenges in the labor market. Government policies that prepare the labor force for retraining and subsidize entrepreneurial activities should be complemented to respond to the evolving labor market.

4. Pilot Programs: Launching pilot projects in sectors like electronics and automotive can showcase the tangible benefits of industrial robots. These examples can inspire more companies to adopt similar technologies by demonstrating efficiency gains, quality enhancements, and supply chain robustness.

Conclusion

Global trade dynamics are experiencing a seismic shift with a surge of industrial policies targeting critical sectors, such as the electronics and automotive industries. As companies search for more resilient supply chains, we have observed a sharp increase in industrial robot adoption in China, led by initiatives such as Made in China 2025. Although South Korea’s GVC participation has increased in recent years and GVC positioning is changing, new adoption of industrial robots has been relatively slowly embraced. To remain competitive in critical manufacturing sectors, South Korea needs government subsidies for increased robot adoption and research. At the same time, a disruption in the labor market is inevitable. Hence, government policies that support re-training and self-employment must be complemented by ongoing efforts to strengthen South Korea’s economy.

Sunhyung Lee is an Assistant Professor of Economics at the Feliciano School of Business, Montclair State University. The views expressed here are the author’s alone.

Photo from Shutterstock.

KEI is registered under the FARA as an agent of the Korea Institute for International Economic Policy, a public corporation established by the government of the Republic of Korea. Additional information is available at the Department of Justice, Washington, D.C.

link