Humanoid robots are accelerating their entry into factories. Guotai Haitong Securities pointed out that material handling and quality inspection are the preferred paths for their commercialization. The core challenge lies in the return on investment; to achieve payback within two years, the price of the robots needs to drop to the tens of thousands of yuan range. Although ‘brains’ and ‘dexterous hands’ remain technological bottlenecks, with the scaled application by CATL and the entry of automobile manufacturers, the market potential for industrial scenarios in China is expected to exceed 48 billion yuan by 2035.

Humanoid robots are rapidly becoming a reality in factories, starting to assume the role of the ‘new generation of blue-collar workers.’

The latest milestone comes from the battery giant $CATL (03750.HK)$ . According to an official announcement by CATL, the world’s first new energy power battery PACK production line to achieve large-scale implementation of humanoid embodied intelligence robots has officially commenced operations at its Zhongzhou base. The humanoid robot, named ‘Xiao Mo,’ is now capable of precisely completing the final functional testing process for battery packs before they leave the production line, a task that involves high-voltage risks.

The introduction of ‘Little Mo’ is regarded as a ‘milestone breakthrough in the application of embodied intelligence in smart manufacturing.’ According to official disclosures, its plug-in success rate remains consistently above 99%, its operational rhythm has reached the level of a skilled worker, and its daily workload has tripled. This successful case provides critical empirical evidence for humanoid robots transitioning from laboratories to real, complex industrial production lines.

The introduction of ‘Little Mo’ is regarded as a ‘milestone breakthrough in the application of embodied intelligence in smart manufacturing.’ According to official disclosures, its plug-in success rate remains consistently above 99%, its operational rhythm has reached the level of a skilled worker, and its daily workload has tripled. This successful case provides critical empirical evidence for humanoid robots transitioning from laboratories to real, complex industrial production lines.

This progress is not an isolated case but rather confirms the general trend identified in industry analysis. In a recent in-depth research report, Guotai Haitong Securities noted that humanoid robots are in the initial stages of commercial deployment, with their application following a progressive strategy from simple to complex tasks. The report emphasizes that, for the market and investors, the key at this stage is to observe their economic viability and technological maturity in specific scenarios, rather than expecting them to immediately replace human labor entirely.

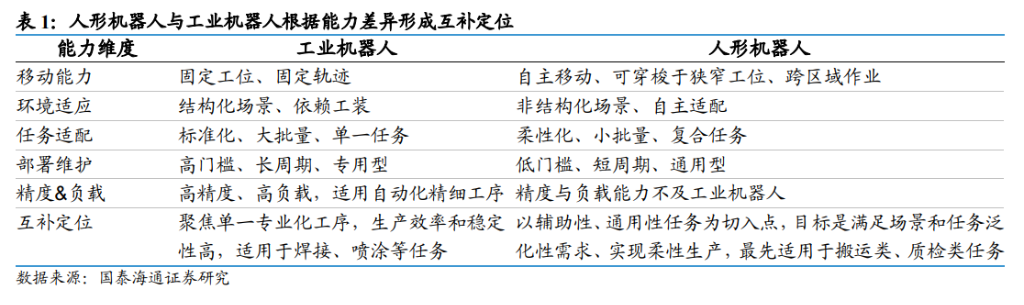

From Complement to Integration: The Complementary Positioning of Humanoid Robots and Industrial Robots

The introduction of humanoid robots into factories does not aim to directly replace highly automated industrial robots but rather to fill the gap between traditional automation equipment and manual labor.

Guotai Haitong Securities’ report explicitly states, ‘Humanoid robots are not intended to replace industrial robots but aim to replace manual workstations.’ The two will form complementary roles: industrial robots will continue to focus on high-speed, high-load, and precise repetitive tasks at fixed stations, while humanoid robots will leverage their flexibility and mobility advantages.

Their complementarity is reflected in the following:

-

Mobility: Industrial robots are fixed at workstations, whereas humanoid robots ‘possess autonomous mobility capabilities, enabling them to navigate narrow workstations and perform cross-regional operations.’

-

Environmental Adaptation: Industrial robots rely on ‘structured scenarios,’ whereas humanoid robots can ‘accommodate unstructured scenarios and autonomously adapt.’

-

Task Adaptation: Industrial robots are suitable for ‘standardized, large-scale’ tasks, while humanoid robots are adaptable to ‘flexible, small-batch, and multi-tasking operations.’

The report argues that in the short term, the manufacturing sector will adopt a model of ‘human decision-making + industrial robot precision execution + humanoid robot flexible integration.’ Factories, due to their ‘more structured working environments,’ will become the ideal ‘training ground’ for humanoid robots, with further deployment into households and commercial settings once the technology matures. In industrial contexts, the report specifically highlights that ‘wheeled forms, with advantages in stability, long battery life, and high-speed mobility, will become the preferred choice for industrial applications.’

Implementation Roadmap: Prioritizing material handling and quality inspection, with basic assembly underway.

The report notes that during the initial implementation phase, humanoid robots will start with ‘short-chain tasks,’ continuously accumulating operational data to train and enhance their capabilities.

The report suggests that humanoid robots will ‘initially excel at material handling and quality inspection tasks.’

This is because such tasks ‘generally exhibit semi-flexible characteristics, involve significant human participation, and have not yet been fully replaced by traditional automated equipment.’ Additionally, they are ‘short-chain and relatively independent processes,’ aligning with the current development status of embodied intelligence. Examples include flexible loading and unloading in stamping workshops and parts sorting and delivery in final assembly workshops.

Regarding ‘basic assembly tasks, such as preliminary screw tightening, component pre-installation, emblem mounting, and wiring harness connections, humanoid robots are currently in the initial testing phase.’

Notably, in industrial settings, the form factor of robots is equally important. The report asserts that ‘wheeled configurations, which offer advantages in stability, long battery life, and fast mobility, will become the preferred choice for industrial applications.’ Compared to bipedal forms, wheeled robots achieve higher movement efficiency and lower risk on flat factory floors, better meeting manufacturing requirements for stability and continuous operation.

Core Commercialization Bottlenecks: ROI and Technological Challenges.

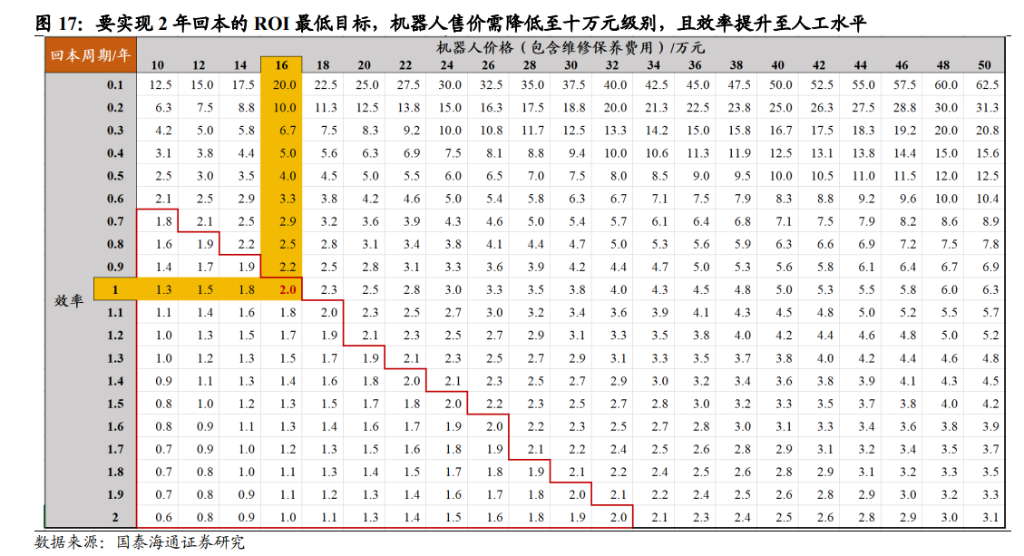

Despite the gradual clarification of application scenarios, large-scale commercialization of humanoid robots still faces two core obstacles: economic feasibility and technological bottlenecks. For any enterprise, the decision to introduce new equipment ultimately boils down to return on investment (ROI).

A report by Cathay Pacific Haitong Securities conducted calculations, pointing out that ‘ROI determines commercial implementation; to achieve the minimum goal of a two-year payback period, the price of robots needs to be reduced to the 100,000-yuan range, with efficiency increased to match human labor.’ The report noted that the current prices of humanoid robots used in industrial settings mostly fall within the 300,000-500,000 yuan range, significantly higher than the target price of 160,000 yuan (assuming annual labor costs of 80,000 yuan and a two-year payback period). This implies that the industry chain must achieve significant cost reductions through technological iteration, scaled mass production, and supply chain optimization.

At the technological level, two bottlenecks stand out.

First, ‘the development of embodied intelligence remains lagging, with insufficient capability to handle complex, multi-step tasks.’ Current humanoid robots still struggle to complete intricate processes requiring multi-step coordination without human intervention, as their task generalization and autonomous decision-making abilities remain in the early stages.

Second, ‘fine manipulation capabilities need improvement, with the durability, flexibility, and force control of dexterous hands being another major hurdle in transitioning from demonstration to practical use.’ In tasks requiring precise hand-eye coordination, such as assembling small parts or connecting cables, robots’ capabilities still lag far behind those of human hands.

Additionally, the report highlights an important direction: ‘In some developed countries with labor shortages and high labor costs, the commercial loop for humanoid robots could be completed first, making overseas markets a potential key focus.’ Report data shows that by 2025, the average hourly wage for warehouse workers in the U.S. will be $23.99, while the estimated operating cost for Agility Robotics’ Digit robot is only $10-12 per hour, demonstrating significant economic benefits.

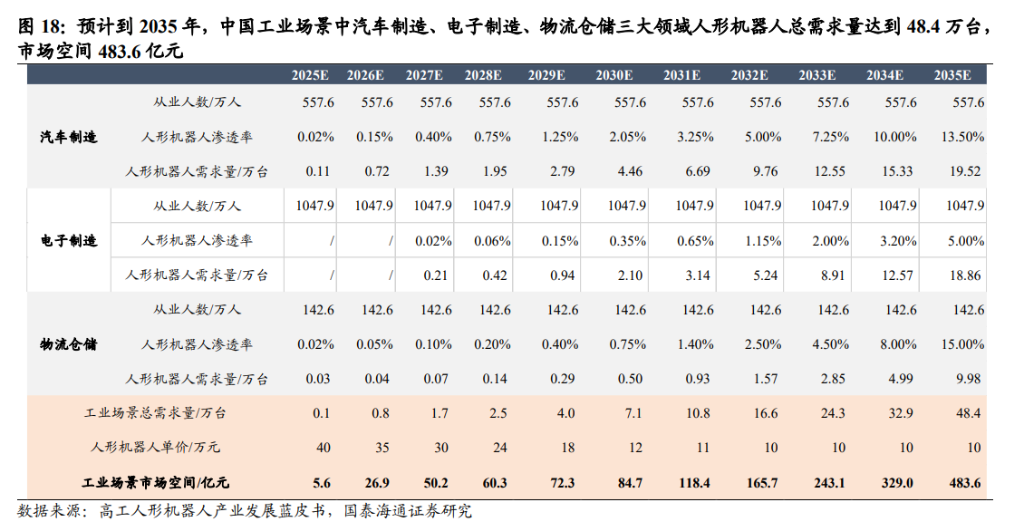

48 Billion Yuan Market Outlook: Synergistic Progress Between Automakers and Robotics Companies

Despite the challenges, the prospects of humanoid robots in the industrial sector are still widely optimistic, driven primarily by addressing global labor shortages and replacing dangerous environment operations. The report forecasts that by 2030, there will be a labor gap of nearly 8 million workers in the global manufacturing industry.

Based on this, Cathay Pacific Haitong Securities has provided a quantified market projection: ‘By 2035, the total demand for humanoid robots in China’s industrial sectors—automotive manufacturing, electronics manufacturing, and logistics warehousing—is expected to reach 484,000 units, with a market size of 48.36 billion yuan.’ This forecast outlines significant growth potential for investors.

In this transformative phase, automakers are playing a crucial role. The report emphasizes that $Tesla (TSLA.US)$ 、 $XPeng (XPEV.US)$ companies such as XPeng Motors possess both technological and application scenario advantages, driving the deployment of humanoid robots in industrial settings.”

Tesla, XPeng, and other vehicle manufacturers are able to extend their technological expertise and supply chain advantages in the intelligent vehicle sector to humanoid robots, with the ability to initially trial and validate these technologies within their own automotive production lines.

These enterprises can not only repurpose AI, perception, and control technologies accumulated in the intelligent vehicle domain for use in robotics but also directly provide the most valuable application scenarios and training data within their own factories.

-

Tesla Optimus: Already being tested in factories for tasks such as sorting batteries, with plans to establish a larger-scale third-generation humanoid robot production line by 2026.

-

XPeng IRON: Has entered its own factory to participate in automotive production training and aims to achieve scaled mass production of advanced humanoid robots by the end of 2026.

In addition, collaboration between humanoid robot manufacturers and automobile companies is becoming increasingly close. For instance, Figure’s humanoid robots from the U.S. have been undergoing in-depth pilot programs at BMW Group’s factories. According to Brett Adcock, founder of Figure, their Figure 02 robots have participated in the production of 30,000 vehicles at BMW’s plants over the past six months, accumulating more than 1,250 hours of operation. These pioneers’ explorations are providing invaluable experience for the commercialization path of the entire humanoid robotics industry.

link